Pay with points: unlocking loyalty program value

The term ‘pay with points’ implies that a customer can burn loyalty points or miles at a point of sale as the method of payment. That means the points have economic value, and can be used to cover the entire purchase amount, or combined with cash to settle the payment obligation.

It also implies that the customer can do this quite easily and freely, across a large proportion of a brand’s inventory, in its primary commerce channels. That’s in contrast to being offered a restricted set of inventory items for redemptions via a members’ portal (i.e., the modest number of reward seats that an airline makes available on a flight, or the items curated in a redemption catalog).

Pay with points is trending upward in loyalty marketing for three main reasons.

- Over the past 3-4 years, brands with loyalty programs have been more focused on offering members new ways to redeem points and obtain interesting rewards. This is to increase participation among those less frequent customers who are never going to get to a free flight, hotel stay, or iPad.

- Marketing and payment technologies have now matured to the point where enabling pay with points is far easier and more affordable for brands.

- The current economic situation in most countries is also generating more interest to redeem points easily for basic family needs.

The purpose of this article is to explain the key considerations around pay with points for brands considering incorporating it into their loyalty programs.

In the first section, I will set out why pay with points is a valuable marketing tactic for businesses. In short: it will increase loyalty engagement by enabling greater freedom and choice around redemptions; and, when dynamic value allocation is incorporated, will produce greater ROI.

I will then explain the technical requirements of enabling pay with points – an effort that will be far easier for brands which are already adopting modern loyalty technology.

Finally, I will discuss some best practices around pay with points, which should help deliver the greatest value to customers, and to the business.

How ‘pay with points’ creates value for brands and customers

Brands should be proactively manipulating the value of their points in order to drive desired behavior, while also helping customers get the highest perceived value at the lowest cost for the brand (this is what’s known as dynamic value allocation).

This last sentence is the most important one in this entire article, but I see too few loyalty programs making much effort to achieve this balance; rather, they just follow easier paths that treat all members as equal. As a result, only those customers with very large points balances have traditionally been able to redeem for interesting rewards: since there have been fewer redemption options for less frequent customers.

This is part of the reason that the loyalty industry has trended continually towards greater points liquidity since modern points-based loyalty programs emerged around 40 years ago. The more widely points can be earned and burned, the greater the proportion of customers that can be engaged. This also creates more opportunities to dynamically award points for desired behavior and adapt the value of the points depending on the context of the redemption.

When modern points-based loyalty programs were first launched by airlines about 40 years ago, you could only earn airline miles by flying, and burn those miles on further flights. This means the points were extremely useful in just one specific use-case: with a small number of frequent customers who could reach the redemption threshold. This is an example of a highly illiquid currency: easy to earn, but difficult to spend without considerable frequency with the brand.

Over time, loyalty currencies became more liquid, as brands in more categories sought to engage more customers with increasingly more creative promotions.

This started out with Hertz and Avis issuing 500 miles in your favorite airline loyalty program when you booked a rental car, to hotels doing the same, and then followed by the founding of Air Miles Canada as the first non-travel coalition loyalty program.

The success of Air Miles was due to the fact that customers could allocate a good portion of their monthly discretionary spending to those brands participating in the coalition. This had a massive impact on customer behavior, and the participating brands acquired a great deal of new customers who were interested in the points.

This was followed by AMEX and other credit card schemes funding points out of their interchange fees on card spend. In most cases, the points earned from credit card companies could be transferred into popular airline or hotel loyalty programs, as well as redeemed for products/services aggregated by the card scheme operator.

This evolution over 30 years introduced greater liquidity in points-based schemes. Customers steadily gained more options for earning among partners, and more choice as to where that loyalty value could be transferred or spent.

However, it wasn’t until the past 10 years that brands started enabling what we might now call ‘pay with points’. There were predecessors, but the technical solutions could not really operate at scale – in part because of constraints with the point of sale (POS) or payment terminals at retail locations. Examples of these less-successful solutions were introduced by Visa or Mastercard. Under these schemes, the customer would receive a message following a card purchase, asking if they wanted to settle the obligation with their balance of points.

The first implementations of pay with points at scale took place with customers being able to link their AMEX, Citi, or Chase accounts with Amazon in the USA. Once an account was linked, Amazon customers (and members of the card scheme loyalty programs) could apply their balance in points, at a value defined by the card schemes, toward the cost of a purchase. Hilton and a few other programs also started working with Amazon.

Most recently, we have seen AMEX points becoming available in Australia as a method of payment on Myer’s online sales channel – so this trend is starting to expand worldwide.

I believe this evolution will continue. With modern technology to enable loyalty commerce at scale, and online or offline payment terminals that can accept many more methods of payment (crypto, loyalty points, virtual cards, etc.), loyalty program operators can now give their customers much more choice in how they extract value from the loyalty program.

In fact, what looks like a gradual evolution in the loyalty industry, over the past 40 years, has significant parallels in how other types of marketplaces have evolved over thousands of years. We wrote an article on the evolution of marketplaces a while ago and you can see many similarities.

Currency Alliance was specifically created based on the observation that loyalty commerce would continue to evolve in this way. Customers would be given more choice in how they earn points among a much larger mix of partners, and how those points could be redeemed through exchanges to other programs, or be spent across a wide variety of partners.

While points or miles have always been considered a type of eMoney or stored value, only recently has the industry been treating them as an asset class with similar characteristics to money. That is a good thing, since the more liquid points become, the more desirable they are to collect in the first place – which increases customer engagement.

The driving force of this evolution is market competition. Brands recognize that only motivating their most frequent customers is no longer enough – and that failing to incentivize other customers is limiting a loyalty program’s effectiveness and total ROI.

I estimate there are over $500B USD worth of loyalty points in circulation worldwide – which is the size of the total economy of Ireland or Norway. About half of that value is probably held by the most frequent business travelers and other high-spenders. These people with lots of points are getting to significant and interesting rewards. But, the other $250B is probably held by another billion people who hold modest numbers of points across dozens of accounts.

You should regard that $500B as a source of untapped revenue for your brand. Every pay with points redemption (like any loyalty transaction) is an opportunity to manipulate the reward value in your favor. Loyalty programs are only relevant to customers (members) if they can extract value. It doesn’t matter if they have earned a lot of points as a big spender, or a less frequent customer; if they cannot extract value, they will be apathetic about participation.

When accepting points as the method of payment, the retailer gets paid in cash for the value of points spent at their business, so they don’t have to worry about converting thousands of points/miles from members into cash – more on this below.

Technology requirements for enabling pay with points

There are three basic requirements – and one highly desirable requirement – for enabling pay with points in your loyalty program, including transactions that take place in partner environments.

- Enabling the transaction. When a customer selects pay with points, you need the ability to identify the loyalty program member at the point of sale (POS), verify that they have sufficient points balance for the transaction, and then trigger the deduction of their points balance. If the customer is spending your partner’s currency, it also needs to trigger a cash transaction between yourself and the partner, so that you receive an agreed exchange rate in cash for the transaction sum in points.

- Functional logic & administration. Where pay with points is enabled across a multi-partner loyalty coalition, brands will need to be able to set the value for each partner currency, agree the cost per point with each partner, deal with foreign exchange rate fluctuations, obtain consistent reporting, and deal with reconciliation and settlement.

- Varying the points value based on the context of transaction. This is the highly desirable requirement – since you could have pay with points without this capability, but at significant opportunity cost. This magical ability to adjust the value of points is what gives brands the ability to personalize engagement and deliver perceived value that exceeds the cost to the brand in enabling customers to redeem for interesting rewards.

- Increasing pay with points partnerships. As new partners are added to your loyalty program, you will want to the ability to quickly enable the above pay with points requirements, and manage and report on those partnerships so that they are optimized for greatest possible ROI.

Where this is taking place in the loyalty market today, it is in most cases difficult, slow, expensive – and is far from reaching its full potential.

The solutions by big companies like Amazon, Myers, AMEX, Chase, Citi (described above) have taken place as one-off, direct integrations between the partners – that typically involve many months and hundreds of thousands of dollars of investment. That is not scalable.

The reason for this is that there are many constraints – both business-imposed, and technical – which restrict how loyalty points value is moved around between entities, even within the same brand.

Examples of these constraints include the inability to spend American Express Membership Rewards Points earned in the USA in any other country. I can’t transfer my American Express points from the USA to my account in Spain, and I cannot spend my American Express points from the USA at Myers in Australia.

These limitations exist because the loyalty programs are operating separate loyalty points banks in each region, and/or when the systems are unable to deal with constantly changing foreign exchange rates, or the limitations of the payment terminal or online payment systems.

Those limitations do not need to exist.

This article is not meant to be about Currency Alliance – but, we built our platform to enable any type of loyalty commerce across any country with any fiat currency, all independent of which fiat currency the loyalty currency is pegged to.

Clients using the Currency Alliance platform to facilitate collaboration with partners do not have to use all the features. They can choose to configure their partner collaborations, countries of operation, exchange rates, and underlying value of the loyalty currency depending on the category of goods/services, channel partner, or any other variable.

The entire objective has been to abstract the complexity of every one of the thousands of loyalty systems in the world, so that any two brands can collaborate under mutually agreed terms without friction. All of this can be managed by businesspeople via a management portal that eliminates the dependency on the IT department or vendors for each change.

This answers the majority of the requirements of pay with points described above. It also makes for simpler, safer operation of pay with points, since no partner needs access to the other’s system for any transaction, as this all takes place in our third-party environment. This means you only have one secure API connection to worry about – rather than dozens.

For example, the second largest bank in the USA uses Currency Alliance to allow their members to spend points directly on travel and entertainment services. Most transactions are modest in value, but we had a transaction last year where a customer redeemed $65,700 in points for a luxury cruise. That is a lot of points.

There is also now dedicated technology available to enable receiving points as payment.

One of Currency Alliance’s collaborators in Australia called PicoLabs, which provides payment terminal functionality worldwide, has developed an application that can enable pay with points on any payment terminal running the Android operating system. The PicoLabs solution can also capture all the SKU detail from the shopping basket without the need to integrate with the POS terminal. Together, we are able to identify loyalty program members at the retail location, enable them to earn points (or bonus points based on specific items purchased), or redeem their points as the method of payment.

Currency Alliance also offers a Universal Points Terminal application that can be used at any online or offline retail location, to accept points from partners as the method of payment. No integrations are required because the application runs as a web app in any browser on any device – and it can be installed and configured in about 30 minutes.

Best practices with pay with points

As alluded to in the historic summary above, business imposed constraints, and technical limitations have evolved considerably over the past 40 years. Unfortunately, many legacy systems and entrenched suppliers to such ecosystems remain fairly inflexible in adapting pay with points capabilities for the way consumers now behave.

Not all of these limitations have been due to technical obstacles. Established operators have in many cases created their own limitations that restrict spending points in order to reduce how, when, and where points can be spent. Historically, such limitations favored their balance sheet at the cost of loyalty program members extracting maximum freedom, choice, and value.

Such restrictions are fair to an extent. Absolute liquidity would undermine the purpose of a loyalty currency since the purpose of the loyalty program is to influence specific behaviors. Indeed, the programs can generate much more value (mostly for themselves) by encouraging customers to redeem for distressed inventory – i.e., flight seats or hotel rooms that will otherwise go unsold.

But the present degree of liquidity across most programs is not sufficient to keep the mid-tail and longer-tail customer engaged. In most loyalty programs, fewer than 20% of total members have at least $25 USD in points value. That means that 80% of customers have only a few dollars.

I have often felt that if a customer does not feel like they can reach $25 per year in loyalty value, they will decide it is not worth participating in the first place. For many businesses, typical customer frequency is just too low to ever reach $25 per year. The only way around this is to partner with complementary brands which will also issue your points, or allow you to issue their points. Issuing someone else’s loyalty points might sound unorthodox, but if these less frequent customers will register and let you remain engaged with communications, then that is a small price to pay.

Furthermore, any points investment – whether in issuing your own currency, or a partner brand’s – can be adapted in order to drive greater ROI.

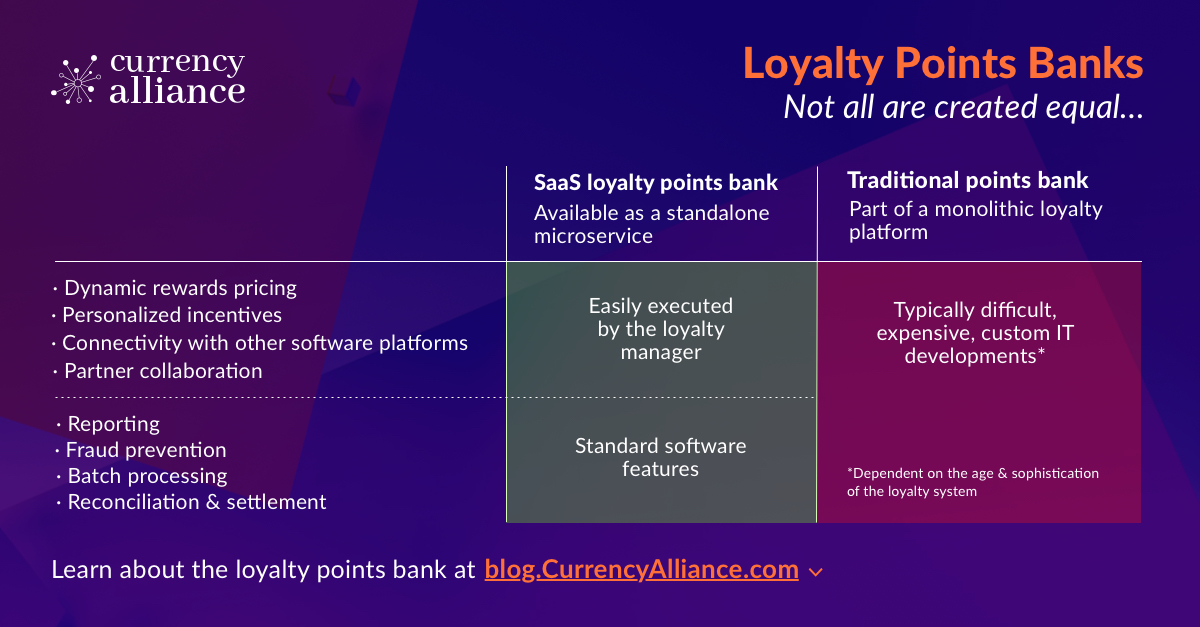

The value of the points being spent/redeemed should vary depending on the context of each transaction – as we discussed in our recent article on the loyalty points bank.

Some loyalty programs already offer customers different values per point/mile depending on how and when they are redeemed – with the specific objective of driving customer behavior that is preferred by the loyalty program operator. For example, if you want to redeem Avios for a flight that British Airways knows is not going to sell out, you normally get twice the perceived value per Avios in such a redemption. The value will be less if you want to redeem your points for merchandise in their e-store, or hotel rewards, or almost anything else – because they want you to redeem for their own services, and not have to pay out cash to a third party supplier or partner.

Similarly, Hilton HHonors points are worth much more when redeemed for hotel rooms than when spent at Amazon with the pay with points feature.

Ideally, however, you want the ability to vary points values more flexibly, drawing on a wider range of data inputs.

For instance, you may publicly announce an offer of 1 point per $1 spent with a partnered retailer – but really, this is only the rate for lower-value customers. If you detect a potentially valuable customer is starting to engage with your brand, you could give a bonus of 2 points per $1 spent. Or, if a particularly valuable existing member puts an item in their cart, you increase the value to 5-10 points per $1 – making them feel even more valued.

*

Another upward trend in loyalty is across-the-board devaluations of loyalty currencies – which have been happening more frequently the past 4-5 years.

This is partly a symptom of the same problem: of customers holding large points balances which they can’t use, producing large liabilities on brands’ balance sheets. But it’s highly detrimental to customer loyalty. Members will have invested months or sometimes years in accumulating points in order to get to an aspirational reward. When a brand devalues those points, the customer can feel violated by the brand.

Points can certainly be devalued, but rather than devalue them across the board, a forward-thinking company will apply dynamic values to the points depending on how they are redeemed – and by whom. In this way, the brand can maintain the perceived value of points for important (loyal) customers and trim the value for those customers/members that have demonstrated themselves to be more fickle.

Consumers are driven by rational and irrational motives, and what is interesting about loyalty points, is that customers may know how many points they have, but they don’t bother to figure out what those points are worth. Therefore, a brand can encourage customer behavior by using pay with points to drive irrational behavior.

Such variations could also be triggered based on the previous action that the customer took if you are trying to get the customer on a path to maximize lifetime value (LTV).

Loyalty programs in this decade need to be focused on maximizing LTV and not focused only on the last transaction or the next transaction with the customer. For this reason, the context of each touchpoint with the customer might dictate giving them extra value or lesser value in order to get the customer to take the next step in building the relationship to increase LTV.

There is an almost infinite range of possibilities for varying points value across your own, or your partners’ inventory. Loyalty program leaders should be highly proactive in setting values for their loyalty currency depending on the context of each transaction because it has a significant impact on program profitability and working capital (cashflows).

Pay with points can be an excellent mechanism to deliver these adjustments across a large ecosystem of partners at scale.

Optimizing customer value and ROI for your points investment

Technology has matured to the point where there are few barriers to creating ecosystems where customers can earn or redeem points across a broad network of complementary brands.

What we are seeing major brands do today is reminiscent of how the Western Union Telegram network was built in 19th century – where the only communications that could take place were between entities directly connected to the wire. A modern solution takes advantage of the infinite connections on the internet to allow every merchant to participate. You could also compare the revolution when Visa introduced its first payment network in the 1950s. Through 70 years of iteration and considerable competition from other payment networks, customers can now make purchases seamlessly with most payment methods across nearly all companies.

Like a country’s central bank, the brand issuing the loyalty points or miles is largely in control over the value of those points depending on how they are redeemed. Fiat currencies like Dollars, Euros, Pesos, Dirham, or others are controlled by governments, and while a country can allow the value of their fiat currency to appreciate or depreciate relative to other fiat currencies, loyalty points are controlled entirely by one company.

That company has much more control over the value of their points/miles. Some companies are good stewards of enhancing customer value, while others will rob the points bank when they need to prop up their balance sheet to meet short-term investor expectations. If your members know they have more freedom to spend your points, they might allocate more of their patronage to you in order to earn more points. Or, they would be interested in earning more of your points among partners that are also willing to issue them.

What could be more interesting to think about is how your business could accept loyalty points from dozens of other loyalty programs that become your partners, so their members can use that value to acquire your products or services.

Loyalty points have always represented a form of economic value, but until recently, that value was obscure and, in many cases, difficult for customers to spend.

We now, however, live in a world where many customers view loyalty points as a new asset class with real economic value. Brands should take advantage of that and help customers get maximum value. In doing so, you will build more loyalty and grow the business.

Pay with points is a valuable tool to give customers more freedom and choice in how they engage with your brand, and an effective tool for managing program liability to improve program results.

Enable Pay with Points in your loyalty program

As mentioned, enabling pay with points in your loyalty program will be much easier if you operate modern loyalty software.

Our recent two-part series on the core modules that make up a loyalty platform:

- the loyalty points bank: when sourced as an SaaS microservice, it frees up your ability to issue your currency at any customer touchpoint, including with partner brands

- the loyalty rules engine: which can be used to vary points issuance and value based on the context of the transcation.

You can read articles on the points bank here and the rules engine here – or visit CurrencyAlliance.com to learn more about software.