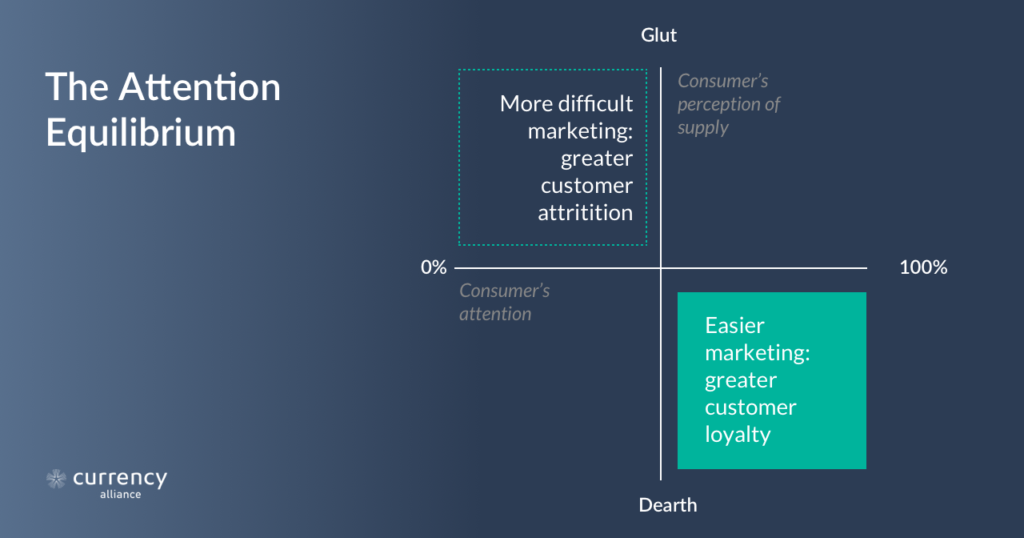

The Attention Equilibrium

People have often talked about consumer attention being a commodity.

People have also talked about the problem of industrial oversupply.

The two are inextricable.

Jean-Baptiste Say, who proposed the theory that supply creates its own demand, understood that supply and demand exist in a state of equilibrium – and that “for every good that is too abundant, there must be another that is too scarce.”

You can display the attention vs. supply equilibrium like so.

Retail ecosystems traditionally managed the issue of oversupply through stockpiling: limiting production and supply of goods, relative to demand, in order to sustain viable profit margins.

But this only worked when oversupply was the only problem.

Since the 1980s, not only has this problem worsened along the whole supply chain – with gluts of commodities, cheaper manufacturing and fast, cheap deliveries to doorsteps – but attention has come under unprecedented demand due to advances in marketing technology.

There are now countless new, more effective, more targeted ways to zero in on peoples’ attention.

To make matters worse, a new breed of company has arisen which capitalizes on this shift in the equilibrium.

Silicon Valley brands stake their entire business models on being chronic over-suppliers.

This has stretched consumer’s attention – and with it, traditional retailers’ business models – to breaking point.

From annoying, to insufferable

Consumers have always felt pestered by brands.

As early as 1759, writer Samuel Johnson complained that “advertisements are now so numerous that they are very negligently perused”.

The difference now is that advertising – like other commodities – is no longer in limited supply.

Whereas advertising slots used to be expensive, digital media has flooded the market with cheap real estate, placing greater demand on attention.

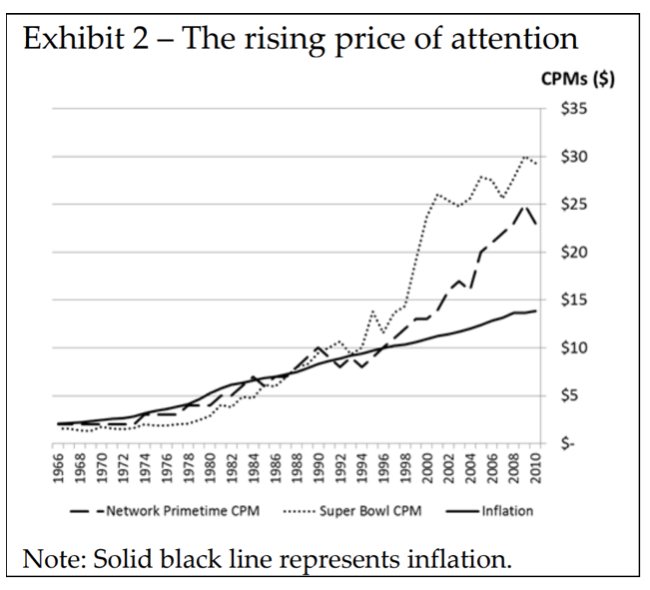

Dr. Thales Texeira, in his essay, The Rising Cost of Human Attention, undertook quantitative analysis of historical costs of television ad conversions, relative to inflation.

Brands experience this in the deflation of advertising dollars: spending more money on increasingly fragmented pieces of advertising real estate, and getting less back.

(A penny for a Google click sounds cheap, but 20 years ago, that’s a penny you’d never have spent).

Consumers, in turn, experience this as an ever-increasing volume of lower quality marketing, as brands clamour to stuff ever more messaging down our necks.

The full severity of this problem becomes apparent at the macroeconomic scale.

It’s now far more difficult to turn a profit on physical goods.

One report from Business Insider indicates that, “online commerce typified by Amazon is making the supply and distribution of goods so cheap that “Amazonisation” itself is now a deflationary force at a macro level”.

And on the digital side, HSBC economist James Pomeroy writes of the “Spotify Problem” – arguing that the increase in digital services puts downward pressure on prices.

To put it simply, advertising, physical goods and digital products are all in a state of glut.

The whole retail ecosystem has been devalued by a perfect storm of oversupply.

Information dumping

Professor Tim Wu, of Columbia Law School, argues that “the attention economy, be it in print, in broadcasts or online, will always incentivize a race to the bottom because that’s where the money is.”

Races to the bottom are a staple feature of competitive markets.

At their most extreme, they manifest themselves as “commodity dumping” – one notable recent example being the purported dumping by China of cheap steel onto Western markets, which put British firm Redcar Steel out of business.

In the Attention Equilibrium, the race to the bottom is one which technology companies are uniquely positioned to win.

Big tech brands operate as their own supply ecosystems: sufficiently independent to be able to manage their own equilibria of demand and supply – with little or no risk of being undercut by a competitor.

Amazon, for instance, has its own delivery network, its own retail technology and now its own acquisitions of high-street stores.

The tech sector as a whole turns “demand for labor on and off like a light switch”, patching tiny gaps in the labor markets with micro-jobs.

And in the case of companies that deal in digital goods, they are effectively their own supply chains, trading data, eyeballs and media within highly productive walled gardens that only they control.

With few or even no suppliers to pay, technology brands can always set the lowest possible price for people’s attention, taking a hit on margins that no other business model could withstand.

Unfortunately for conventional retailers, humans appear to be gluttons for punishment.

In November 2017, an Economist briefing on the influence of social media on politics noted the “now-ubiquitous pull to refresh feature, which lets users check for new content, has turned smartphones into slot machines.”

This is only the beginning.

Facebook plots an information dump on a totally unprecedented scale – beaming free 5G internet down from the sky – and is making good progress.

This must serve as a warning to any retailer planning to step further into the digital fray.

You’re pitting yourself against Silicon Valley.

These businesses are monopoly-holders and master innovators in the art of over-supply: hijacking consumers’ reward pathways at a macroeconomic scale, increasing demand on peoples’ attention with a supply of information of infinitesimal quality and value, which seeps into every last crack to the point of saturation.

Pick your battles.

My bet is, this is one you won’t win.

No brands please, we’re exhausted

Nonetheless, conventional retailers seem oblivious to the hopelessness of the challenge.

In almost all cases, they are attempting to reshape their business models to also become over-suppliers.

“The pricing pressure has ignited intense wargaming inside the largest CPG companies, according to people familiar with discussions at Procter & Gamble, Unilever, PepsiCo, Mondelez and Kimberly-Clark…

“It’s dominating the conversation every week,” said an executive at one of these companies.

Representatives for these companies either declined to comment or failed to respond to requests for comment. “

As consumers, we experience this in the almost-permanent state of discounting in stores and endless irrelevant media placements online.

As business owners, we experience it in the time we’ve spent adapting our businesses to regulations such as GDPR, designed to mitigate the barrage of communications to which we’re subjecting our endlessly-harangued patrons.

Thales Texeira recognises the problem:

“The price of attention is rising because demand for attention is outpacing its supply… At the same time, attention quality suffers as more money spent by more advertisers means more “shouting” in the marketplace. Consumers in turn respond by covering their eyes and ears more often.”

Frustratingly, however, Texeira falls into the same trap as the majority of thought leaders who have twigged the attention economy, but not the Attention Equilibrium.

He advises an “attention-contingent advertising strategy” whereby you either:

- advertise less

- advertise in ways that demand less attention

- ensure that you capture more attention.

This will not work, because as I discussed earlier, advertising too is now an oversupplied commodity – and the competitive “race to the bottom” will prevail.

If you advertise less, somebody else will pay less for your spot.

If you demand less attention, someone else will pay less to demand more.

If you try to capture more attention, the more it plays into Silicon Valley’s hands.

Partners in adversity

For a brand such as Walmart to view a brand such as Facebook as a competitor requires a leap of thinking, but it offers two crucial benefits.

Firstly, it shines a light on the circularity of the Attention Equilibrium, as opposed to a one-directional information economy.

Paraphrasing Jean-Baptiste Say, The Economist writes that, in order to get to grips with demand and supply, you need to make an “intellectual jump… from micro to macro, from a worm’s eye view of individual plants and specific customers to a panoramic view of the economy as a whole.”

Your own spiralling ad spend, and your plummeting customer experience, is not necessarily entirely your fault, but a consequence of bigger forces which exist outside of your control.

This makes it easier to understand that scrapping around in isolation for solutions, or deploying tactics such as Texeira recommends, may only dig yourself deeper into trouble.

That realization, in turn, paves the way for the second benefit: the adoption of a highly-productive siege mentality by traditional retailers.

A “panoramic view of the economy as a whole” should help brands, who previously had no common ground, to see themselves as partners in adversity.

A “panoramic view of the economy as a whole” should help brands, who previously had no common ground, to see themselves as partners in adversity.

For a revealing analogy: in The Secret Life of the Cat, a BBC documentary series, it was revealed that moggies who live in close urban quarters operate a schedule.

They have an unwritten rule to patrol the neighborhood at different times: Tom leaving the house between 12 and 1, for instance, before scurrying home so that Ginger next door can take her turn.

They do this in order to avoid each other.

The success of this system depends on two factors:

- awareness of the problem of limited supply (of mice and fish carcasses, one presumes)

- a mutual willingness to tackle the problem.

In much the same way as the neighbourhood moggies work together to share their own limited space and supplies, brands should work together to claw back their ancestral territory.

Contending with Silicon Valley, it seems improbable they’ll find any other sufficiently weighty weapon with which to reset the scales.

Natural progression

This suggestion is not a drastic deviation, but a natural progression from the status quo, whereby retail ecosystems sustain profits by collaboratively limiting supply relative to demand.

It’s simply that, now that attention is undersupplied, instead of conventional commodities, the ecosystem must adopt a new shape around the new finite resource.

This must occur at the point at which the resource is used, i.e., by the consumer-facing brand.

Walmart may not wish to collaborate with Target, but it could collaborate across verticals, and form productive alliances with Ford. Or Universal Studios. Or Nando’s.

Walmart may not wish to collaborate with Target, but it could collaborate across verticals, and form productive alliances with Ford. Or Universal Studios. Or Nando’s.

This might entail agreeing to timeshare advertising impressions against mutual customers; or collaborating via a platform like ours in order to reward customers for shopping within brands’ chosen networks of co-conspirators.

If the co-conspirators choose to share data, an improved understanding of each individual could reduce spray-and-pray marketing in favor of more accurately targeted messaging.

Demand on attention becomes alleviated – and the risk of competitors filling the gaps becomes mitigated, because other brands are working with you towards the same common cause.

Who knows – a virtuous circle of customer loyalty may ensue.

Customer experience

In truth, many brands turn a profit off very little attention.

The luxury sector, for instance, thrives on precisely the opposite: a notion of superiority and exclusivity.

“LVMH, which owns Celine, Dior, Givenchy, Louis Vuitton and several other luxury labels, recently said it won’t be working with Amazon anytime soon.”

The Engadet article goes on to say that, “For luxury brands, having full control of the retail experience is paramount.”

As soon as you allow Amazon – or any other prevailing market force – to dictate the terms of your business, you surrender that control.

Curiously enough, Silicon Valley brands are themselves, in a sense, low-attention businesses.

“Amazon doesn’t do content marketing.”

Instead, it captures search traffic as it falls and guide it through PPC into their walled garden.

And I must confess, as a consumer, its service is superb.

Data-centric companies such as Facebook, meanwhile, demand minuscule slices of attention: not through headline-grabbing special offers, but through mass-scale fragmentation to the nth degree.

Consumer brands, whose margins rest almost entirely on product mark-ups, will struggle to mirror these successes. Luckily, if they are interested in online marketing this UK digital marketing agency might be able to help them reach their consumers through PPC management and other types of marketing strategies.

Target’s recent acquisition of Shipt was a smart move, but most brands cannot seriously contemplate following in Amazon’s footsteps: diversifying revenue streams by investing in acquisitions and engineering arms, let alone providing such a broad and compelling product offering.

Forging new ecosystems in collaboration with other brands, however, might help traditional retailers wield more clout, enough to at least partly offset the effects of this equilibrium imbalance.

Working together to provide better customer experience, and by agreeing not to trip over each other’s toes in the process, seems like one sensible alternative to endless panicked meetings about Amazon’s latest throw of the dice.

The alternative is not a pretty future for consumer brands.

As long as they keep trying to score points – off each other, and off the battle-weary consumer – the Attention Equilibrium will move forever further in favor of big tech.

~

Are your consumers switching off?

Currency Alliance may be able to help.

We help consumer-facing brands forge alliances, easily and inexpensively, in order to drive greater customer loyalty.

Our free, simple, cost-cutting SaaS tech platform can be used to issue, buy, sell or exchange loyalty currencies with other brands.

This helps brands turn dormant points into profit, whilst customers enjoy the freedom to earn and spend their points with a wider network of brands.

To discover the full range of benefits, explore the platform and find out more at CurrencyAlliance.com.

References:

1 https://www.economist.com/news/economics-brief/21726050-third-brief-our-series-looks-reasoning-made- jean-baptiste-say

2 https://www.wsj.com/articles/global-glut-challenges-policy-makers-1429867807

3 https://www.mckinsey.com/industries/consumer-packaged-goods/our-insights/supply-chain-4-0-in- consumer-goods

4 http://www.hbs.edu/faculty/Publication%20Files/14-055_2ef21e7e-7529-4864-b0f0-c64e4169e17f.pdf

5 http://uk.businessinsider.com/amazon-effect-inflation-deflation-2017-10

6 http://uk.businessinsider.com/spotify-problem-for-economists-2016-9

7 https://medium.economist.com/has-our-attention-been-commodified-abc178e34826

8 http://www.telegraph.co.uk/finance/commodities/11878679/Chinas-dumped-steel-leaves-UK-industry- facing-fight-for-survival.html

9 uk.businessinsider.com/amazon-effect-inflation-deflation-2017-10

10 https://www.economist.com/news/briefing/21730870-economy-based-attention-easily-gamed-once- considered-boon-democracy-social-media

11 https://www.recode.net/2017/6/29/15894640/facebook-drone-aquila-test-flight-landing

12 https://www.recode.net/2017/3/30/14831602/amazon-walmart-cpg-grocery-price-war

13 http://uk.businessinsider.com/walmart-strategy-to-compete-with-amazon-is-paying-off-2017-8? r=US&IR=T

14 http://www.hbs.edu/faculty/Publication%20Files/14-055_2ef21e7e-7529-4864-b0f0- c64e4169e17f.pdf

15 https://www.economist.com/news/economics-brief/21726050-third-brief-our-series-looks-reasoning-made- jean-baptiste-say

16 https://www.engadget.com/2016/10/25/amazon-fashion/ 17 https://blog.kissmetrics.com/competing-with-amazon/

18 https://www.forbes.com/sites/elyrazin/2018/01/04/acquiring-shipt-is-a-smart-move-but-will-it-be-enough- to-help-target-catch-up-with-amazon/#3e0a8371626e